Basic Budgeting

One of management’s major responsibilities is planning—which is the process of establishing company-wide objectives. A successful organization makes both long-term and short-term plans. These plans set forth the objectives of the company and the proposed way of accomplishing them.

A budget is a formal written statement of management’s plans for a specific future time period, expressed in financial terms.

A budget normally represents the primary method of communicating agreed-upon objectives throughout the organization.

Once adopted, a budget becomes an important basis for evaluating performance. It promotes efficiency and serves as a deterrent to waste and inefficiency.

Budgeting and Accounting

Accounting information makes major contributions to the budgeting process. From the accounting records, companies can obtain historical data on revenues, costs, and expenses. These data are helpful in formulating future budget goals.

Normally, accountants have the responsibility for presenting management’s budgeting goals in financial terms. In this role:

- They translate management’s plans and communicate the budget to employees throughout the company.

- They prepare periodic budget reports that provide the basis for measuring performance and comparing actual results with planned objectives.

The budget itself, and the administration of the budget, however, are entirely management responsibilities.

The Benefits of Budgeting

The primary benefits of budgeting are:

- It requires all levels of management to “plan ahead and to formalize goals on a recurring basis.

- It provides “definite objectives for evaluating performance at each level of responsibility.

- It creates an “early warning system for potential problems so that management can make changes before things get out of hand.

- It facilitates the “coordination of activities within the business. It does this by correlating the goals of each segment with overall company objectives. Thus, the company can integrate production and sales promotion with expected sales.

- It results in greater “management awareness of the entity’s overall operations and the impact on operations of external factors, such as economic trends.

- It “motivates personnel throughout the organization to meet planned objectives.

A budget is an aid to management; it is not a substitute for management. A budget cannot operate or enforce itself. Companies can realize the benefits of budgeting only when managers carefully administer budgets.

Essentials of Effective Budgeting

Effective budgeting depends on a “sound organizational structure. In such a structure, authority and responsibility for all phases of operations are clearly defined.

Budgets based on research and analysis should result in realistic goals that will contribute to the growth and profitability of a company. And, the effectiveness of a budget program is directly related to its acceptance by all levels of management.

Once adopted, the budget is an important tool for evaluating performance. Managers should systematically and periodically review variations between actual and expected results to determine their cause(s). However, individuals should not be held responsible for variations that are beyond their control.

Length of the Budget Period

The budget period is not necessarily one year in length. A budget may be prepared for any period of time. Various factors influence the length of the budget period. These factors include:

- the type of budget,

- the nature of the organization,

- the need for periodic appraisal, and

- prevailing business conditions. For example, cash may be budgeted monthly, whereas a plant expansion budget may cover a 10-year period.

The budget period should be long enough to provide an attainable goal under normal business conditions. Ideally, the time period should minimize the impact of seasonal or cyclical fluctuations. On the other hand, the budget period should not be so long that reliable estimates are impossible.

The most common budget period is one year. The annual budget, in turn, is often supplemented by monthly and quarterly budgets.

Many companies use continuous 12-month budgets. The budgets drop the month just ended and add a future month. One advantage of continuous budgeting is that it keeps management planning a full year ahead.

The Master Budget

The term budget is actually a shorthand term to describe a variety of budget documents. All of these documents are combined into a master budget.

The master budget is a set of interrelated budgets that constitutes a plan of action for a specific time period.

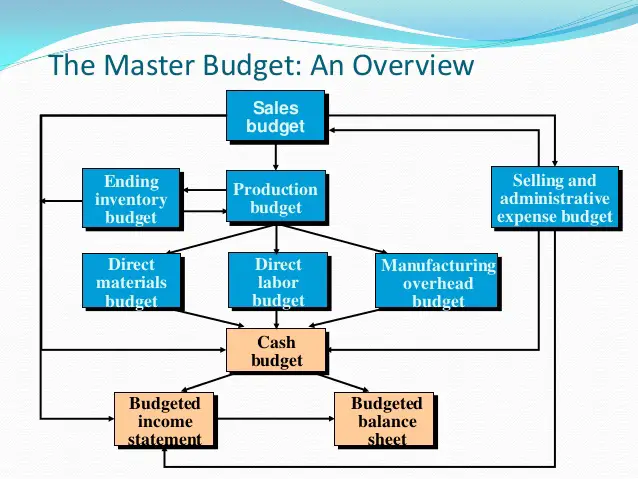

The master budget contains two classes of budgets:

- Operating budgets are the individual budgets that result in the preparation of the budgeted income statement. These budgets establish goals for the company’s sales and production personnel.

- Financial budgets, in contrast, are the capital expenditure budget, the cash budget, and the budgeted sheet.

These budgets focus primarily on the cash resources needed to fund expected operations and planned capital expenditures. Figure X-1 shows the individual budgets included in a master budget, and the sequence in which they are prepared.

Figure X-1. Master Budget. Credit: SlideShare.

Figure X-1. Master Budget. Credit: SlideShare.

The organization first develops the operating budgets, beginning with the sales budget. Then it prepares the financial budgets. These budgets are important to discuss, however, they are beyond the scope of this literature.

You Might Also Like:

- Research data for this work have been adapted from the manual:

- Managerial Accounting: Tools for Business Decision Making By Jerry J. Weygandt, Paul D. Kimmel, Donald E. Kieso