The Balanced Scorecard

The Four Perspectives of the Balanced Scorecard

A recent control system innovation is to integrate financial measurements and statistical reports with a concern for markets and customers, as well as employees.

The balanced scorecard (BSC) is a comprehensive management control system that balances traditional financial measures with operational measures relating to a company’s critical success factors.

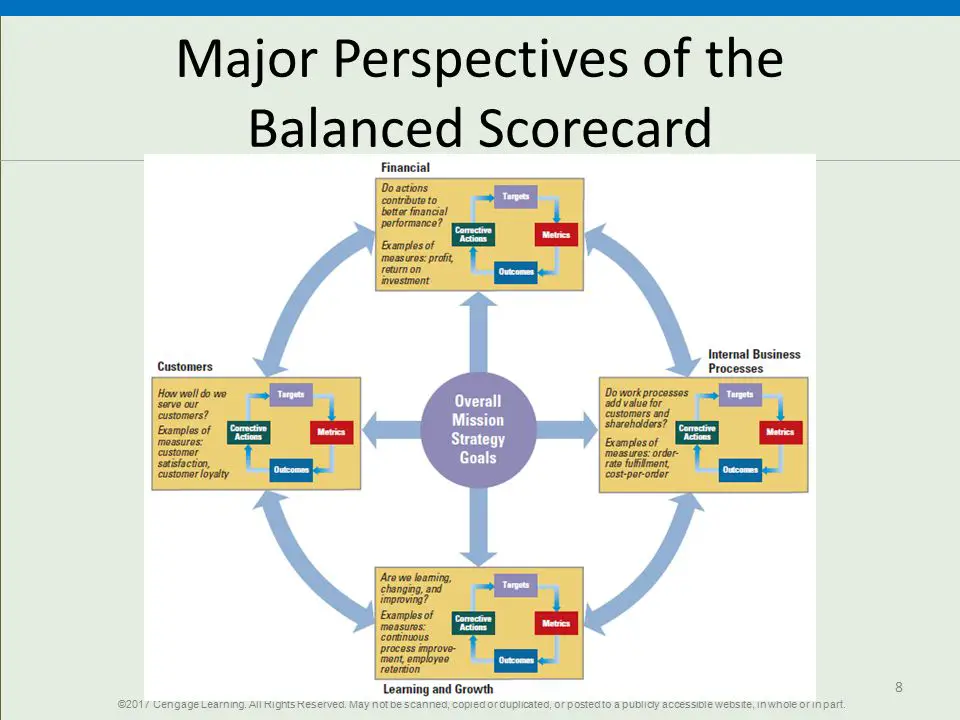

A BSC contains four major perspectives, as illustrated in Figure X6: financial performance, customer service, internal business processes, and the organization’s capacity for learning and growth.

Figure X6 | Major Perspectives of the Balanced Scorecard | Source: SlideplayerOpens in new window

Figure X6 | Major Perspectives of the Balanced Scorecard | Source: SlideplayerOpens in new window |

Within these four areas, managers identify key performance indicators (KPIs) the organization will track.

- The financial perspective reflects a concern that the organization’s activities contribute to improving short- and long-term financial performance. It includes traditional measures such as net income and return on investment.

- Customer service indicators measure such things as how customers view the organization as well as customer retention and satisfaction.

- Business process indicators focus on production and operating statistics, such as order fulfillment or cost per order.

- The final component looks at the organization’s potential for learning and growth, focusing on how well resources and human capital are being managed for the company’s future.

Measurements include such things as employee retention, business process improvements, and the introduction of new products. The components of the scorecard are designed in an integrative manner so that they reinforce one another as illustrated in Figure X6 by lining short-term actions within each of the four perspectives to each other and to the overall mission, strategy and goals. Managers can use the scorecard to set goals, allocate resources, plan budgets, and determine rewards.

Although these elements sound like they apply most clearly to product-based firms, the scorecard can also be applied to both for-profit and nonprofit service organizations.

A large technology service provider, for example, identified KPIs of return on equity (financial), number of ideas implemented within the past year (learning and growth), accuracy and responsiveness (internal processes), and customer loyalty and retention (customer service), among others.

The scorecard has become the core management control system for many service organizations including Hilton HotelsOpens in new window, AllstateOpens in new window, British AirwaysOpens in new window, and Cigna InsuranceOpens in new window. British AirwaysOpens in new window clearly ties its use of the BSC to the feedback control model, which is shown in Figure X5Opens in new window.

Scorecards serve as the agenda for monthly management meetings, where managers evaluate performance, discuss what corrective actions need to be taken, and set new targets for the various BSC categories.

In recent years, the BSC has evolved into a system that helps managers see how organizational performance results from cause-effect relationships among these four mutually supportive areas. Overall effectiveness is a result of how well these four elements are aligned, so that individuals, teams, and departments are working in concert to attain specific goals that cause high organizational performance.

Strategy Map

The cause–effect control technique is the strategy map.

A strategy map provides a visual representation of the key drivers of an organization’s success and shows how specific outcomes in each area are linked.

The strategy map is a powerful way for managers to see the cause–effect relationships among various performance metrics.

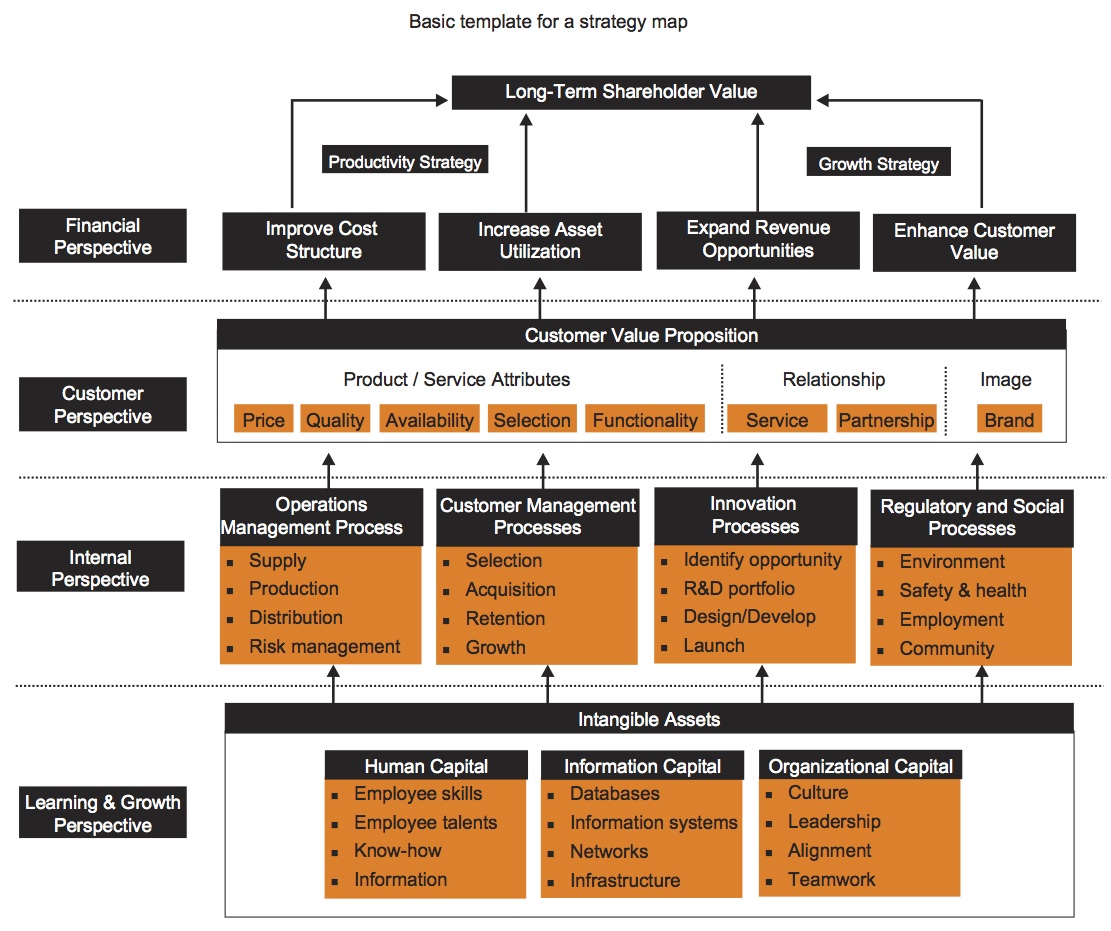

Figure X7 A Strategy Map for Performance Management | Source: InternetOpens in new window

Figure X7 A Strategy Map for Performance Management | Source: InternetOpens in new window |

The simplified strategy map shown in Figure X7 illustrates the four key areas that contribute to a firm’s long-term success — learning and growth, internal processes, customer service, and financial performance — and how the various outcomes in one area link directly to performance in another area.

The idea is that effective performance in terms of learning and growth serves as a foundation to help achieve excellent internal business processes. Excellent business processes, in turn, enable the organization to achieve high customer service and satisfaction, which enables the organization to reach its financial goals and optimize its value to all stakeholders.

In the strategy map shown in Figure X7, the organization has learning and growth goals that include employee training and development, continuous learning and knowledge sharing, and building a culture of innovation.

Achieving these goals will help the organization build efficient internal business processes that promote good relationships with suppliers and partners, improve the quality of flexibility of operations, and excel at developing innovative products and services.

Accomplishing internal process goals, in turn, enables the organization to maintain strong relationships with customers, be a leader in quality and reliability, and provide innovative solutions to emerging customer needs.

At the top of the strategy map, the accomplishment of these lower-level goals helps the organization increase revenues in existing markets, reduce costs through better productivity and efficiency, and grow by selling new products and services in new market segments.

In a real-life organization, the strategy map would typically be more complex and would state concrete, specific goals; desired outcomes; and metrics relevant to the particular business. However, the generic map shown in Figure X7 gives an idea of how managers can use strategy maps to set goals, track metrics, assess performance, and make changes as needed.

You Might Also Like:

- Daniel R. Denison and Aneil K. Mishra, “Toward a Theory of Organizational Culture and Effectiveness,” Organization Science 6, no. 2 (March–April 1995), 204-223.

- Robert E. Quinn, Beyond Rational Management: Mastering the Paradoxes and Competing Demands of High Performance (San Francisco: Jossey-Bass, 1988).

- Mohamed Hafar, Wafi Al-Karaghouli, and Ahmad Ghoneim, “An Empirical Investigation of the Influence of Organizational Culture on Individual Readiness for Change in Syrian Manufacturing Organizations,” Journal of Organizational Change Management 27, no 1 (2014) 5–22.

- Harrison, Michael I. 2005. Diagnosing Organizations: Methods, Models, and Processes. Thousand Oaks, CA: Sage Publications, 29

- Scott, W. Richard, and Gerald F. Davis. 2007. Organizations and Organizing: Rational, Natural, and Open Systems Perspectives. Upper Saddle River, NJ: Pearson-Prentice Hall, 78.

- Jr. 2002. Organization & Management Problem Solving: A Systems and Consulting Approach. Thousand Oaks, CA: Sage Publications, 20.